China Property Signals (#8): A 'Mental Model' For Data Forecasts, Data Distortions

About this Newsletter: Get a quick but finer view of (still) one of the most important sectors in China, with the weekly chart and commentary from Real Estate Foresight (REF) - drawing on 13+ years of REF's research on China housing markets.

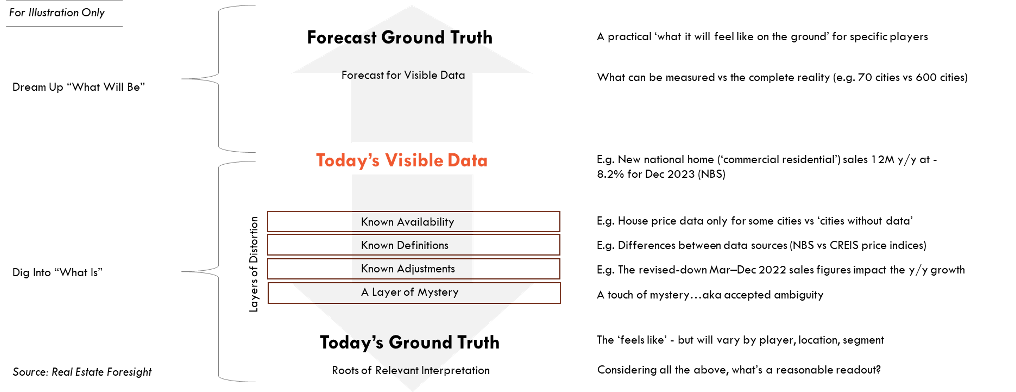

With the Real Estate Foresight China research business, in recent years, we have had more conversations with market participants about the data interpretation and related caveats than the actual views on the market, as well as the differences between 'what the data shows' and 'what it feels like on the ground'.

The schematic below is our attempt to organise the various data issues into a simple framework, with a couple of examples listed:

A 'MENTAL MODEL' FOR DATA FORECASTS - DRAWING ON REF CHINA PROPERTY RESEARCH EXPERIENCE OVER THE PAST 13 YEARS

It's like a map for a deeper data-grounded discussion about the market.

It may appear obvious, but how many forecasts or data readouts explicitly state what they refer to along those dimensions?

This is based on our experience in researching the Chinese housing markets, but the same could apply to any sector, any country.

For China property specifically, we do spend a lot of time just digging into all the nuances of the data.

Some of the current data caveats/'distortions' to watch include:

-Adjustments (explicitly stated) by the NBS to the national new home sales growth figures for certain periods in 2024, which affect any y/y comparisons in 2025.

-When local government entities and state-owned enterprises (SOEs) purchase unsold inventory from developers and acquire a completed or partially completed residential tower-such as one from Evergrande, Kaisa, or Vanke, these transactions could be recorded as contract sales for the developers. Consequently, they may also be reflected in local and national new home sales data.

-A composition change impacting new home price growth indices calculations in some major cities, where new projects tend to be higher-end, pushing the averages up, but at the same time, they might be really selling at a discount to what their theoretical price would have been earlier.

-Simple high-base effects in the y/y comparisons in the past weeks, as we now compare to the Sep-Oct 2024 period, when the major policy support measures were rolled out, with the positive near-term impact. Looked at the other way, the earlier 'less negative' improvement was driven by that late-2024 boost.