China Property Signals (#29): Big Picture Update

About this Newsletter: Get a quick but more granular view of (still) one of the most important sectors in China, with the weekly chart and commentary from Real Estate Foresight (REF) - drawing on 14+ years of REF's research on China housing markets.

There are some positive (or less negative) signs in the most recent weekly China housing market data, with the persistent question, "Have we reached the bottom?"

The rebound in residential sales, prices and inventory improvement in Hong Kong, while driven largely by the Mainland buyers, also contributes to the sentiment, alongside some positive notes from a number of major investment banks.

When we look at the Mainland's monthly macro-property data for March, though, the evidence is not there yet (the April data is due next week).

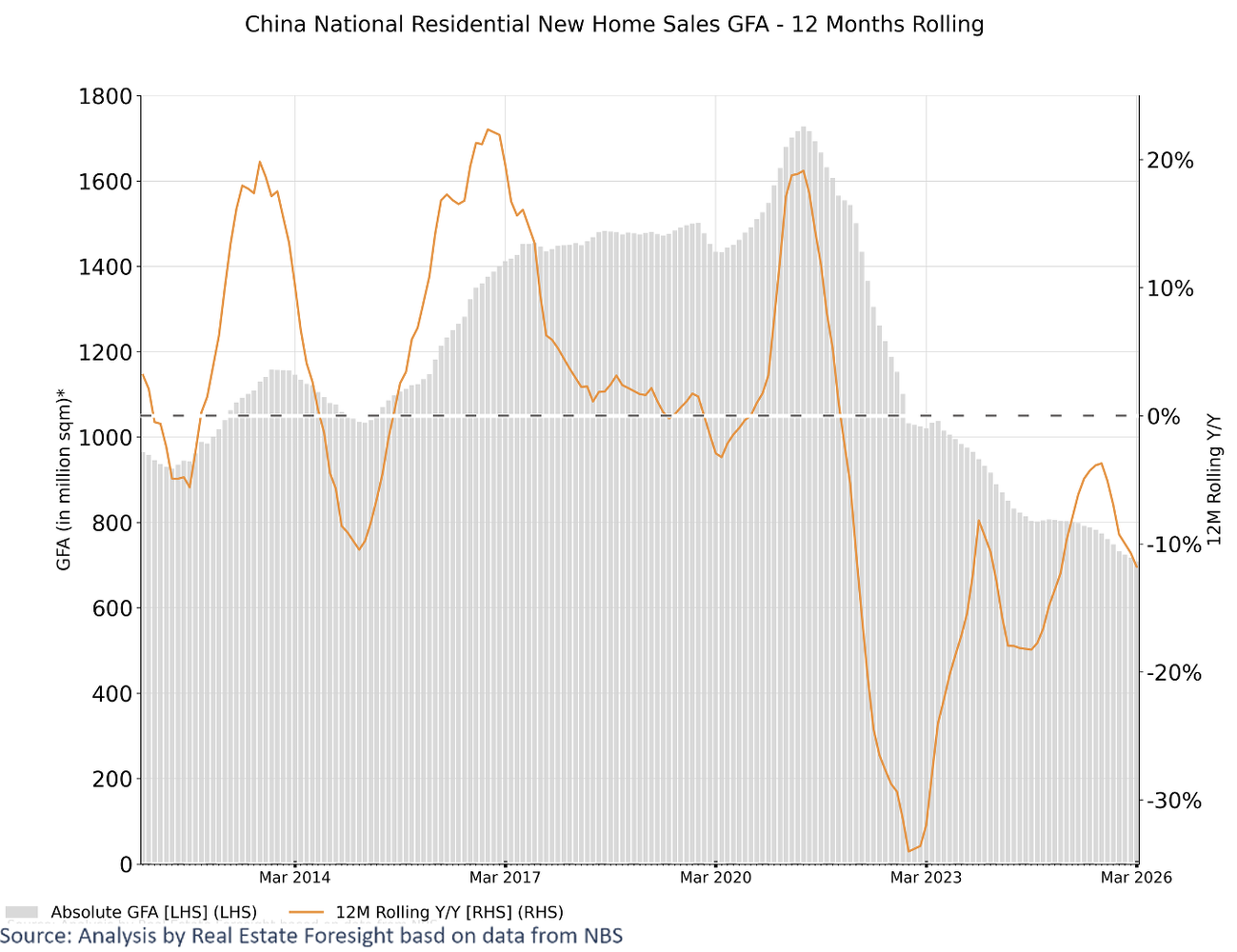

New home sales at the national level (NBS) are now down 59% from the peak in 2021, on a rolling 12-month basis, with the pace of decline extending:

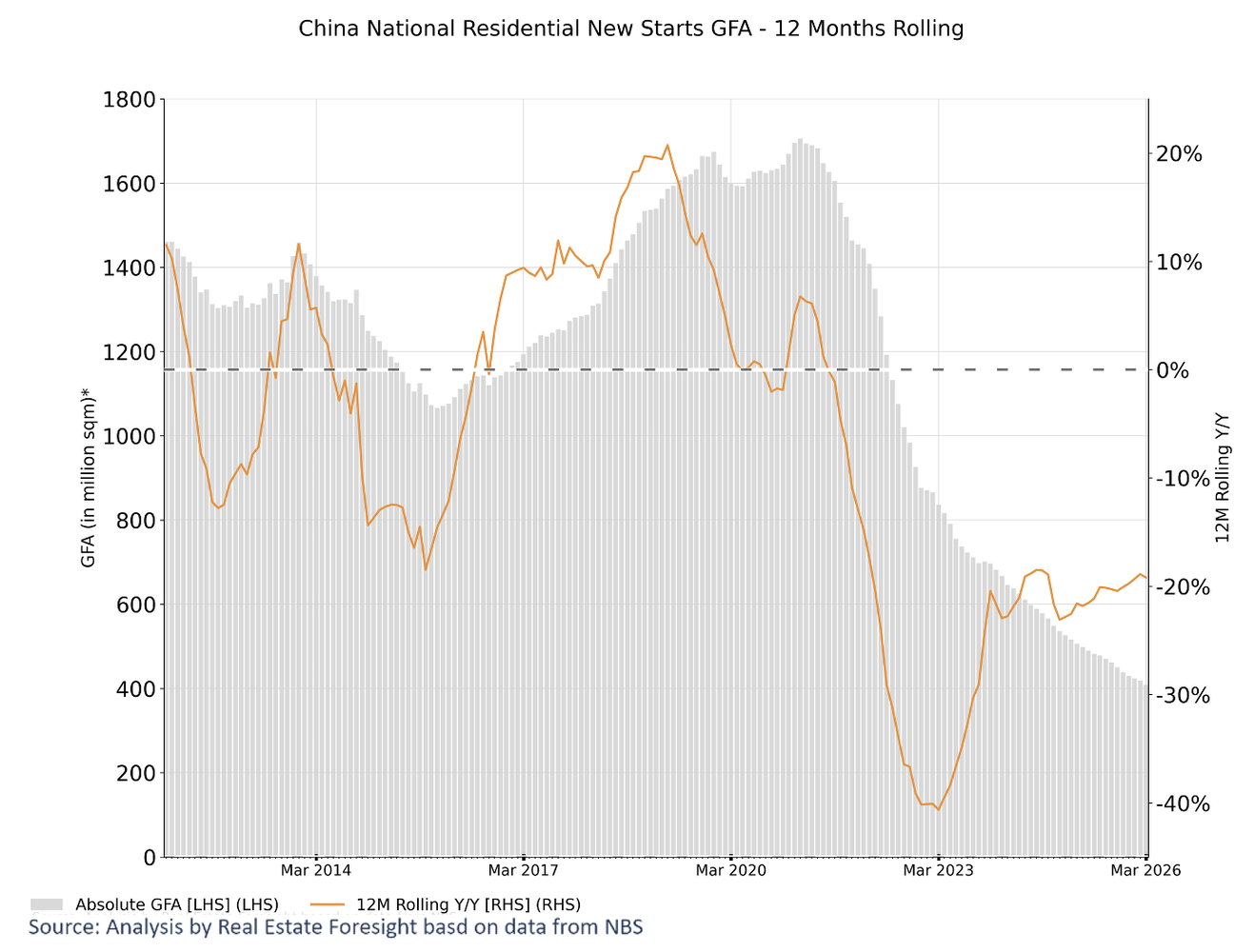

New starts are down 76% from the peak. The 'stability' here is in the pace of annual declines:

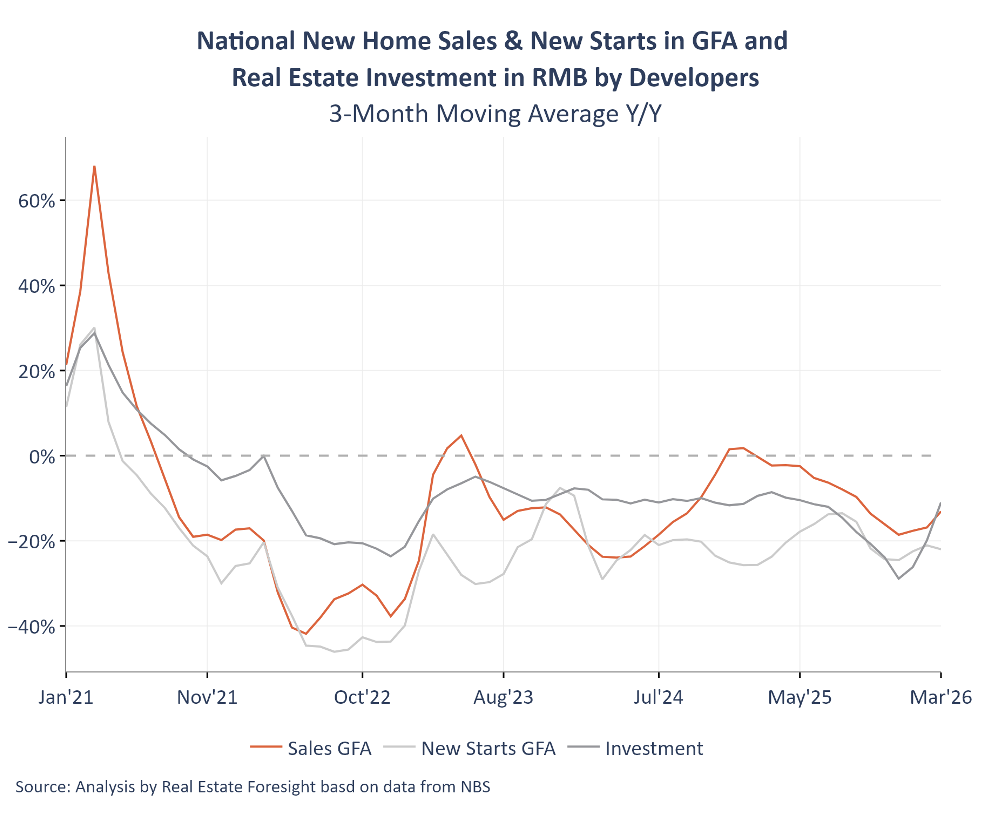

The shorter-term metrics are 'less negative' but it's not yet significant in the context of the past few years:

Now, one could argue that the magnitude of this reset in itself could be a reason to expect improvements.

Which brings the evergreen questions: what should be the normalised annual demand for new homes for China over the next 5-10 years, and, in particular, how will the existing supply of new homes matter and what proportion of housing demand overall can be satisfied through the secondary markets? That's some of the questions we are working on.