About this Newsletter: Get a quick but more granular view of (still) one of the most important sectors in China, with the weekly chart and commentary from Real Estate Foresight (REF) - drawing on 14+ years of REF's research on China housing markets.

We held two small-group in-person meetings this year as part of our 14th Annual China Property Outlook, one in Hong Kong on Jan 29 and one in London (for the first time) on Feb 5.

Continuing the tradition of the 'Draw the Line' survey, here are the results from the small-group forecasts for the national-level new home sales ('commercial residential') in an overlay on one chart:

For comparison, here are the 2022-2025 forecasts vs actuals:

Our main scenario for 2026 new home sales at the national level is -2.5% (vs -9.2% for 2025) and -15% for new starts (vs -19.8%).

At an aggregate level, this reflects China’s new home sales sector continuing to contract into a smaller, healthier, and more rational market. The adjustment remains ‘painful’, with no signs of a rebound, and the very latest data points to further deterioration across most key metrics.

Further policy support is coming, but we assume our ‘Support-not-Stimulus’ theme from 2024 will continue to hold, and the support measures will be just sufficient to gradually improve the major metrics to ‘less negative’.

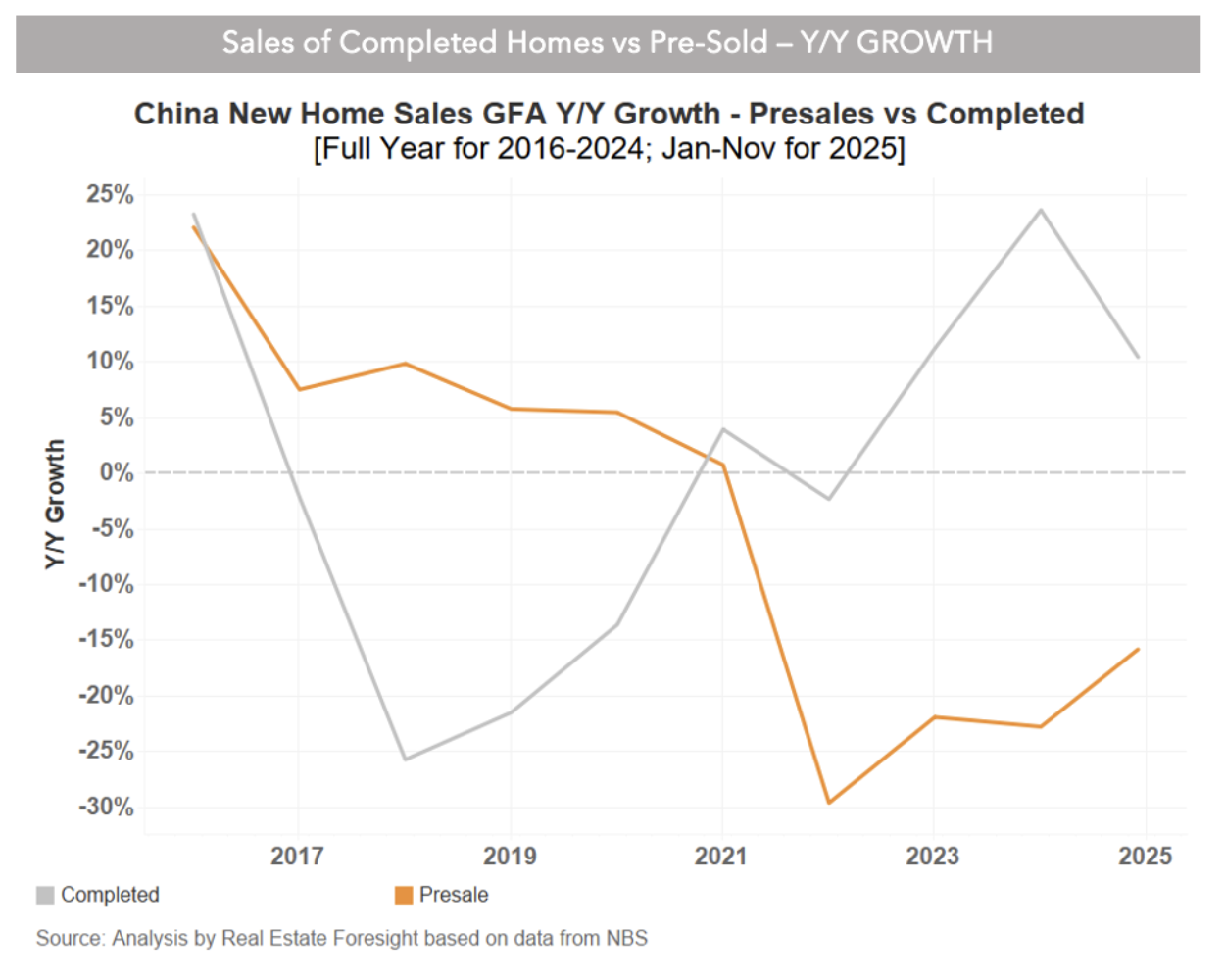

But more importantly, we point out several distinctions. For example, did you know that within the new home sales category, it's the pre-sales that took a big hit, while the sales growth of completed new homes has been positive since 2023:

Other distinctions on our list include:

-Primary (new homes) vs the secondary market

-Delivery progress vs new sales

-Inventory clearing vs inventory levels

-National aggregates vs city- or segment-level trends

-Official data vs data interpretation caveats and the on-the-ground reality checks

-Private developers vs SOEs

-Policy support vs stimulus measures

-Property vs technology macro context (GDP)

-Mainland China vs Hong Kong comparisons